Winter Economy Plan

The Chancellor has published a Winter Economy Plan.

The policy document notes: “A number of the government’s interventions to support jobs and employment – including the Coronavirus Jobs Retention Scheme (CJRS) and the Self-employed Income Support Scheme (SEISS) are due to come to a close over the autumn, while other schemes – such as the Jobs Retention Bonus and employment support including Kickstart Scheme – begin to take effect. The government’s aim through all of these schemes has been to prevent skills from fading, maintain strong employment relationships between workers and firms, and support the self-employed. The new schemes the government is introducing will reinforce that objective, while ensuring that businesses can adapt and evolve to the prolonged challenge of COVID-19. Further technical details of the schemes will be available on gov.uk.”

The plan includes the following announcements (full details below)

- a new six month Job Support Scheme which will operate in tandem with the Job Retention Bonus from November 2020.

- help for the hospitality and tourism sectors through a continuation of the reduction in VAT until 31 March 2020

- an extension to the application period for four government-backed loans schemes, and changes to the terms of repayment for Bounce Back Loans (BBLS) and Coronavirus Business Interruption Loans (CBILS)

- new payment schemes to ease the burden of paying deferred VAT.

CTG Vice-Chairman Richard Bray commented:

“The staggering of the repayment dates for VAT deferred earlier this year could help many charities. But charities will need to opt-in to benefit. Many charities are facing horrendous financial pressures and additional targeted support for the charity sector is critical. We call on the Treasury to properly acknowledge this in the months to come.”

The following measures will apply across the UK (content below reproduced from the policy document)

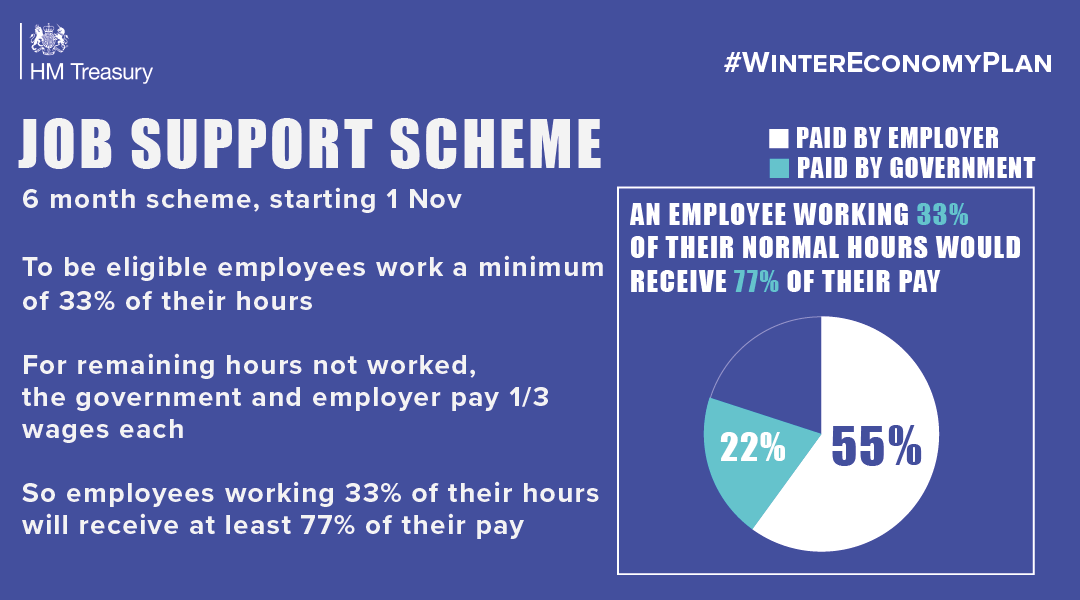

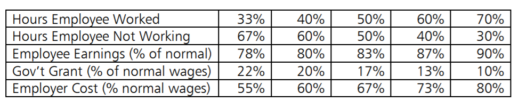

Job Support Scheme – To support viable UK employers who face lower demand due to COVID-19, and to keep their employees attached to the workforce, the government will be introducing a new Job Support Scheme from 1 November 2020. Employees will need to work a minimum of 33% of their usual hours. For every hour not worked the employer and the government will each pay one third of the employee’s usual pay, and the government contribution will be capped at £697.92 per month. Employees using the scheme will receive at least 77% of their pay, where the government contribution has not been capped. The employer will be reimbursed in arrears for the government contribution. The employee must not be on a redundancy notice. The scheme will run for six months from 1 November 2020 and is open to all employers with a UK bank account and a UK PAYE scheme. All Small and Medium-Sized Enterprises (SMEs) will be eligible; large businesses will be required to demonstrate that their business has been adversely affected by COVID-19, and the government expects that large employers will not be making capital distributions (such as dividends), while using the scheme.

A Job Support Scheme Factsheet has also been published and can be read here. It includes examples and further information on the operation of the scheme.

SEISS Grant Extension – The government recognises the continued impact that COVID-19 has had on the self-employed and has taken action to provide support. The SEISS Grant Extension provides critical support to the self-employed. The grant will be limited to self-employed individuals who are currently eligible for the SEISS and are actively continuing to trade but are facing reduced demand due to COVID-19. The scheme will last for 6 months, from November 2020 to April 2021. The extension will be in the form of two taxable grants. The first grant will cover a three-month period from the start of November until the end of January. This initial grant will cover 20%of average monthly trading profits, paid out in a single instalment covering 3 months’ worth of profits, and capped at £1,875 in total. The second grant will cover a three-month period from the start of February until the end of April. The government will review the level of the second grant and set this in due course.

VAT deferral ‘New Payment Scheme’ – The government will give businesses which deferred VAT due in March to June 2020 the option to spread their payments over the financial year 2021-2022. Over half a million businesses deferred VAT payments, a cash injection of £30 billion into the UK economy when it needed it most. Rather than paying in full at the end of March 2021, businesses will be able to choose to make 11 equal instalments over 2021-22. All businesses which took advantage of the VAT deferral can use the New Payment Scheme. Businesses will need to opt in, but all are eligible. HMRC will put in place an opt-in process in early 2021.

Extending the temporary VAT reduced rate for hospitality and tourism – To continue supporting the cashflow and viability of over 150,000 UK businesses and to protect 2.4 million jobs, the government is extending the temporary reduced rate of VAT (5%) from 12 January to 31 March 2021. This will continue to apply to supplies of food and non-alcoholic drinks from restaurants, pubs, bars, cafés and similar premises, supplies of accommodation and admission to attractions across the UK.

Extension of access to finance schemes – The government is extending four temporary loan schemes, which have helped over a million businesses to date, to 30 November 2020 for new applications:

- Bounce Back Loan Scheme (BBLS) – BBLS has provided £38 billion of finance through more than a million loans to UK-based small businesses, many of which had not previously borrowed. Loans are between £2,000 and £50,000, capped at 25% of turnover, with a 100% government guarantee to the lender to provide them with the confidence they need to support the smallest businesses. The borrower does not have to make any repayments for the first twelve months, with the government covering the first twelve months’ interest payments. Under the new Pay as you Grow options (see below), Bounce Back Loan borrowers will all be offered the choice of more time and greater flexibility for their repayments.

- Coronavirus Business Interruption Loan Scheme (CBILS) – CBILS has provided over 66,000 loan facilities worth £15.5 billion to eligible UK-based businesses with turnover under £45 million. The scheme provides loans of up to £5 million with an 80% government guarantee to the lender, giving lenders the confidence to provide finance to SMEs. The government does not charge businesses for this guarantee and also covers the first twelve months of interest payments and fees.

- Coronavirus Large Business Interruption Loan Scheme (CLBILS) – CLBILS has provided more than 566 facilities worth over £3.8 billion to eligible UK-based businesses with turnover above £45 million. The scheme provides loans of up to £200 million (to a maximum of 25% of turnover), with an 80% government guarantee to the lender, which is more generous than equivalent schemes in many other countries.

- Future Fund – Our investment scheme for innovative and fast-growing UK-based businesses, has provided loans ranging from £125,000 to £5 million which are subject to at least equal matching from private investors. Over 700 convertible loans worth £720 million have been approved. Businesses that have already accessed a Future Fund convertible loan cannot apply for another one.

Support also continues through the COVID-19 Corporate Financing Facility which will remain open until 22 March 2021. Where a company has exhausted all other options, and is of strategic importance to the UK, the government may also consider providing bespoke financial support.

Pay as you Grow – The government will give all businesses that borrowed under the BBLS the option to repay their loan over a period of up to ten years. This will reduce their average monthly repayments on the loan by almost half. UK businesses will also have the option to move temporarily to interest-only payments for periods of up to six months (an option which they can use up to three times), or to pause their repayments entirely for up to six months (an option they can use once and only after having made six payments). These changes will provide greater flexibility to repay these loans over a longer period and in a way that better suits businesses’ individual circumstances.

CBILS loan extension – The government intends to allow CBILS lenders to extend the term of a loan up to ten years, providing additional flexibility for UK-based SMEs who may otherwise be unable to repay their loans.

Enhanced Time to Pay for Self-Assessment taxpayers – The government will give the self-employed and other taxpayers more time to pay taxes due in January 2021, building on the Self-Assessment deferral provided in July 2020. Taxpayers with up to £30,000 of Self-Assessment liabilities due will be able to use HMRC’s self-service Time to Pay facility to secure a plan to pay over an additional 12 months. This means that Self-Assessment liabilities due in July 2020 will not need to be paid in full until January 2022. Any Self-Assessment taxpayer not able to pay their tax bill on time, including those who cannot use the online service, can continue to use HMRC’s Time to Pay Self-Assessment helpline to agree a payment plan.